Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

– Definition of internal audit.

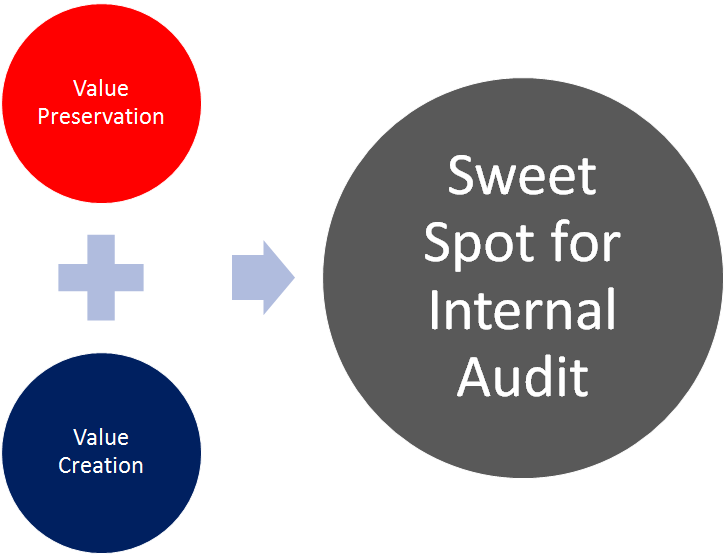

I believe Internal audit has two roles:

- Value Preserver (Police Man Job)

- Value Creator/ enhancer (Adviser role)

I see a paradox in Internal audit’s role.

On one hand management want Internal auditor to be eye and ear of management and do surprise audits (a.k.a. policing). They want Internal audit to advise them on managing tricky issues related to compliance and bringing competitive advantages to organization.

On the other hand, regulators are asking management/ auditors to certify that Internal control exist and effective.

What is the point where Internal audit will find the balance?

I believe that role of value preserver is given. It has to be fulfilled.

Role of value creator can be played only after/ while fulfilling role of value preserver.

Call for action:

Inputs/ comments/ suggestion: I welcome inputs/ comments / suggestions from readers on how to approach this issue. Feel free to correct me, educate me.

Share the Article: If you like it, share it. If you share it with others, and they comment, we all will get more learned.

(Disclaimer: The views expressed constitute the opinion of the author and the author alone; they do not represent the views and opinions of the author ’s employers, supervisors, nor do they represent the view of organizations, businesses or institutions the author is, or has been a part of.)